$40k deposit. $14.66M.

The new budget just made this possible.

The rules have changed. Yes.

“Is property investing dead?”

Wrong question.

The better question:

“What does this make more valuable?”

A strategy we are already reviewing with clients (Case Study)

Single LMI eligble professional earning $135,000+ based in Sydney.

Tailored strategy options for you are available at the end of this email.

Over the past five years, we have helped first home buyers execute this exact structure. The 2026 budget did not break the strategy. It just made it stronger.

The First Time Buyer Just got more powerful.

Eligible first home buyers can enter with a 5% deposit and no LMI.

On an $800,000 purchase, that’s only $40,000 to enter the market.

The property is not the strategy.

Yes, you can buy land in Sydney at this price point. Most people don't believe that. The ones who do, but still don't act, are missing the structure, the team, or both.

Negative gearing is boring. And under the new rules, it’s done.

Buy. Run at a loss. Claim it against salary. Hope growth carries you.

But if these rules pass as announced, the loss no longer drops to your tax return immediately. So the lazy version of negative gearing dies.

The Real Strategy

Buy with a 5% deposit. $800k purchase. $40k deposit. $760k P&I loan.

Live in it for at least 12 months. Satisfy the scheme. Pay principal and interest.

Paying down non-deductible debt at 6% is a guaranteed after-tax return.

No volatility. No CGT event. No fund manager.

For a share portfolio to beat that on an after-tax, after-CGT, short-term basis, it has to do far more than people think.

Move out. Rentvest. Extract every dollar above 90% LVR.

Once the property becomes an investment, you don’t stop paying P&I.

You keep paying it down.

But every time equity above 90% LVR builds, through capital growth or principal reduction, you extract it as a new Interest Only (I/O) split.

That split is investment debt.

Invested into income-producing shares.

The interest is fully deductible against your salary today.

That part. The new rules did not touch.

Repeat. For 30 years.

The property is no longer just a property.

It is something that transforms your life.

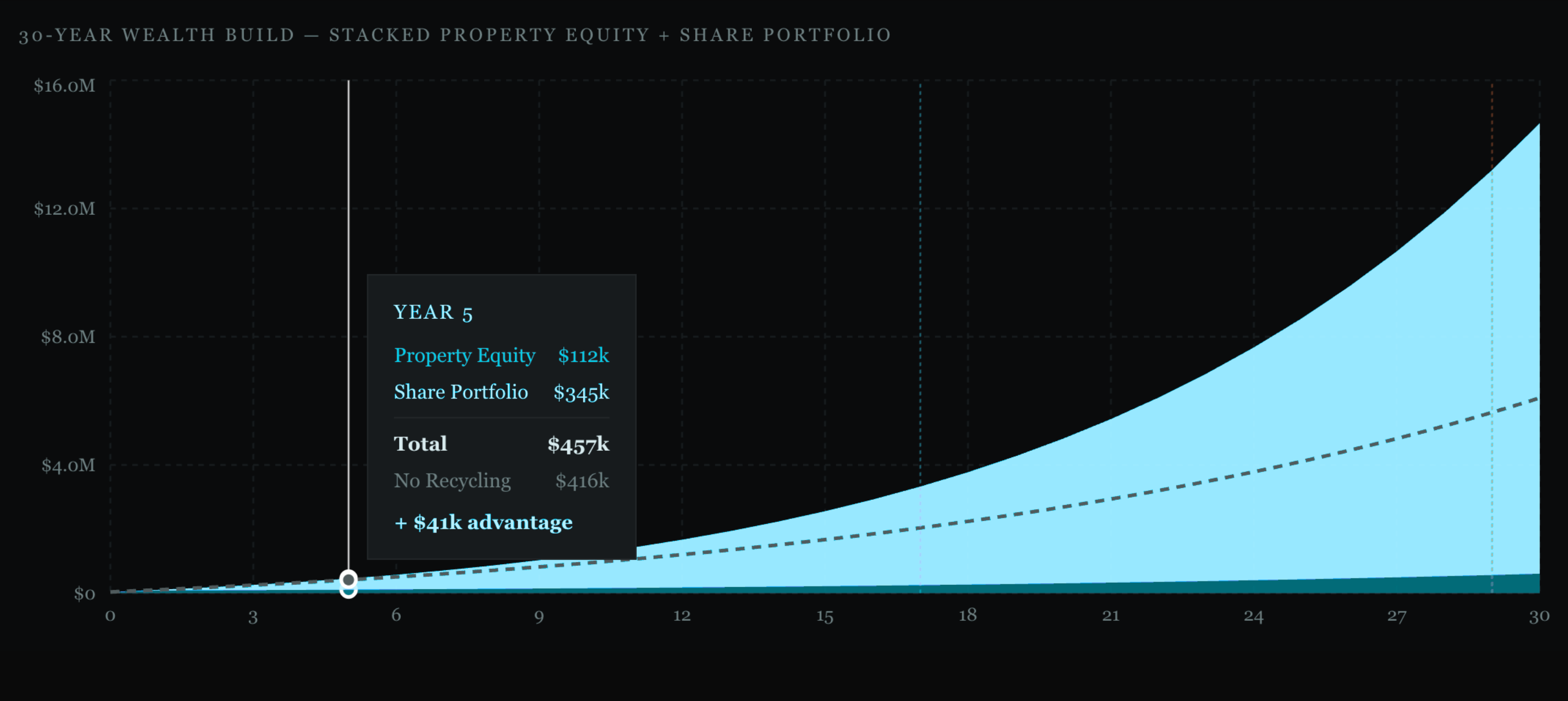

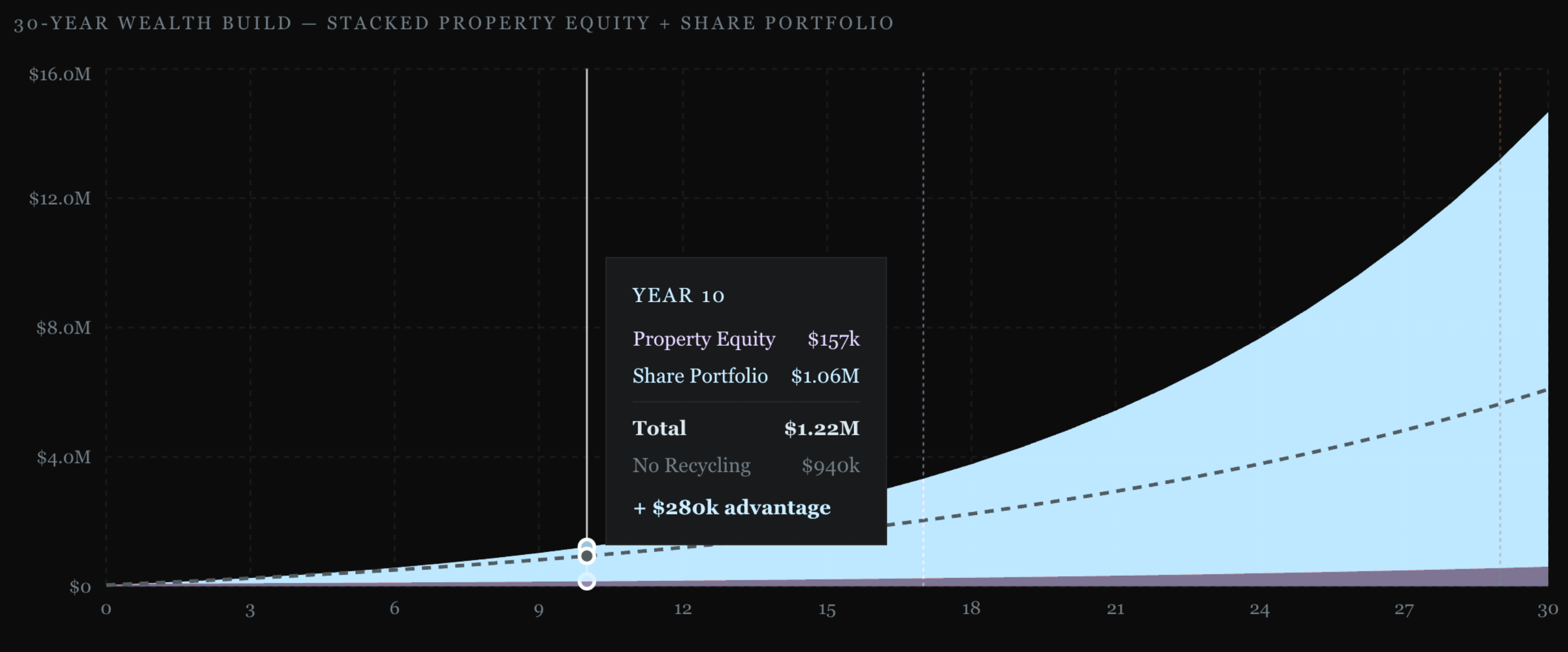

The Wealth Journey

Net Wealth: $1,220,000

From a $40k deposit.

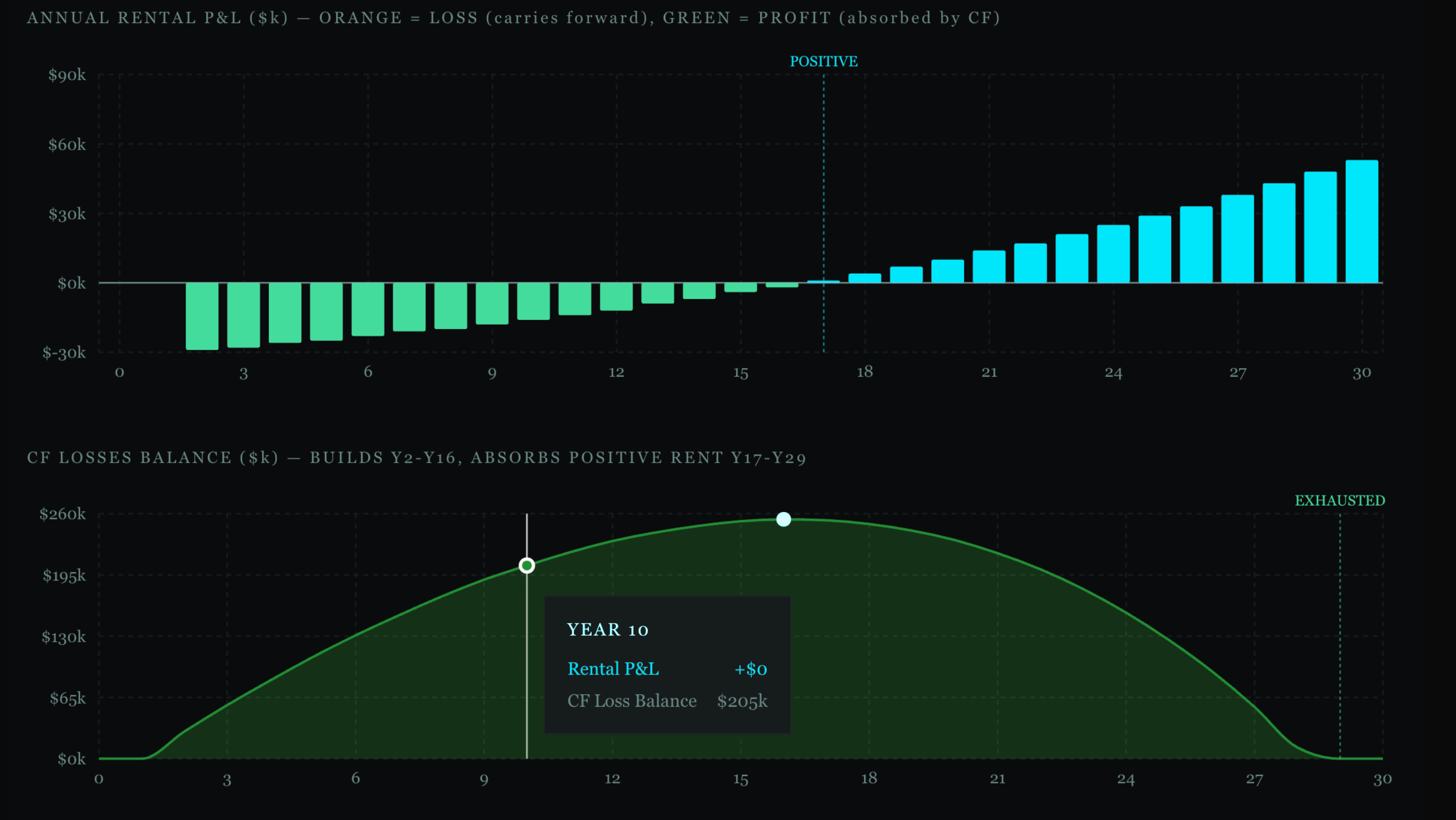

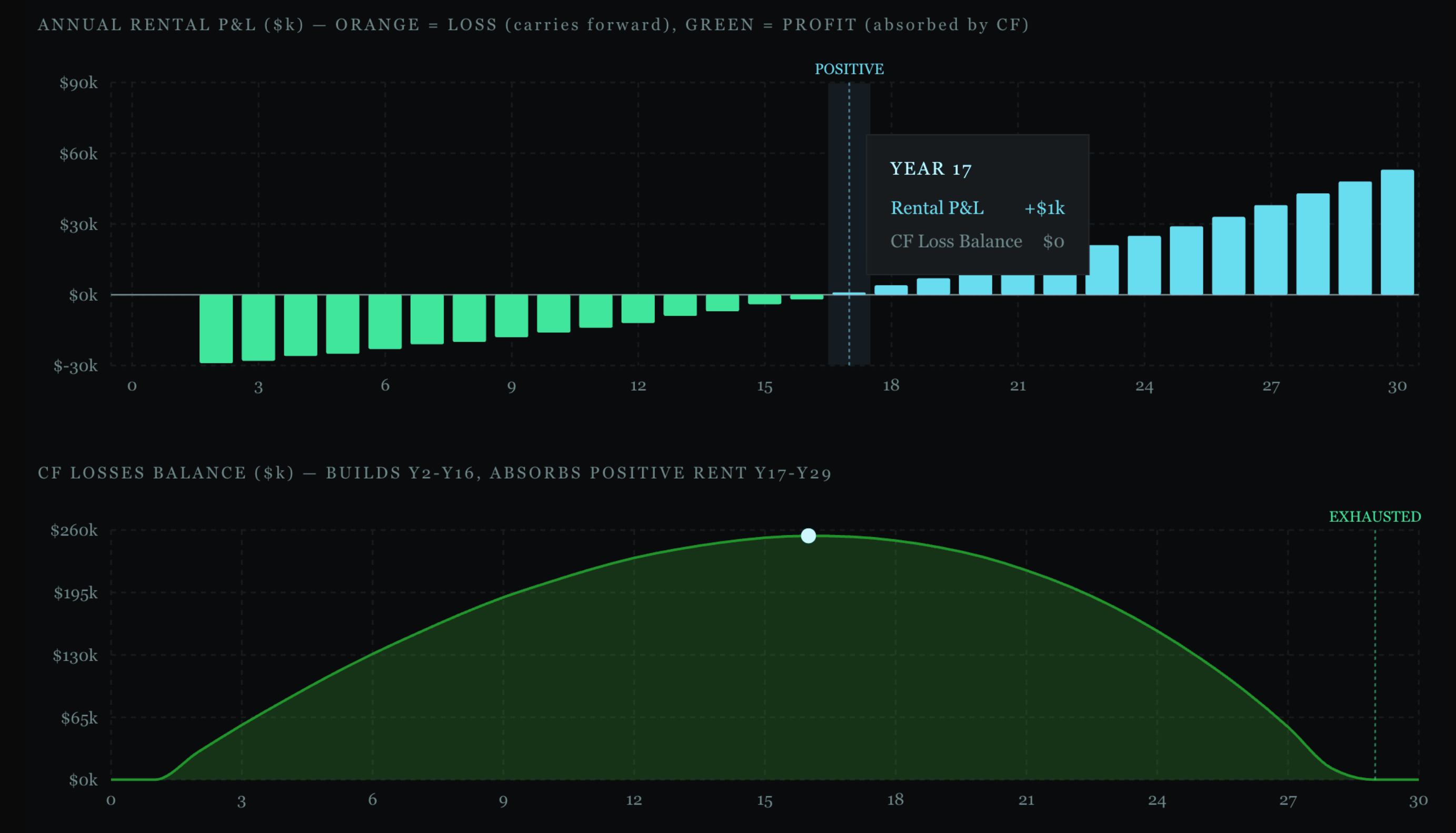

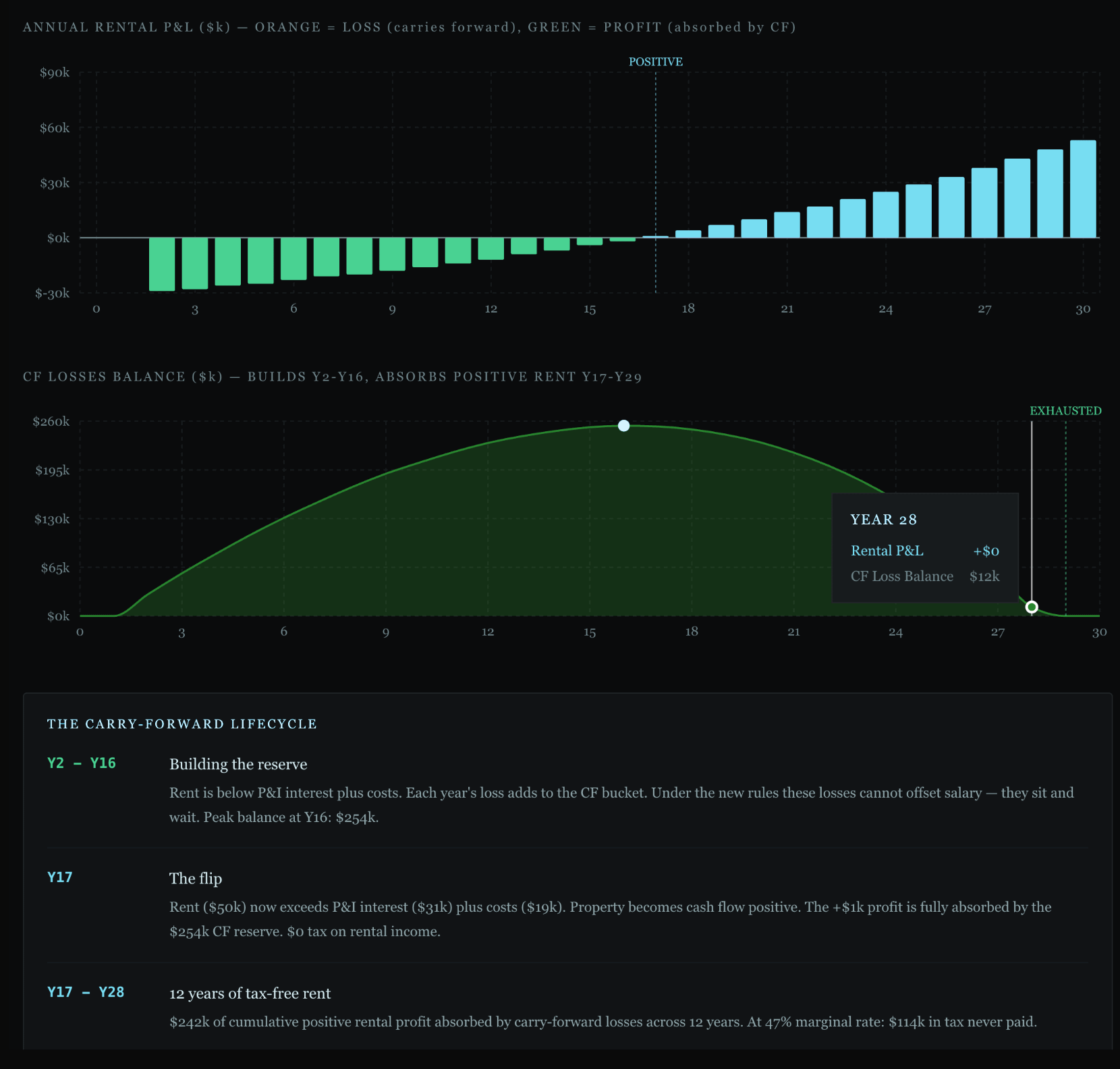

And $205k of carried-forward rental losses are sitting in reserve, banked under the new rules. (Rental loses offset future rental profit)

This is where the real magic of the new strategy begins.

Rent ($50k) finally exceeds P&I interest ($31k) plus costs ($19k).

The property turns cash flow positive for the first time.

But the profit is not taxed.

|Because the $254k of carried-forward losses absorbs it.

For 12 consecutive years (Y17 through Y28), the property delivers positive rental income that is absorbed tax-free by the banked losses.

$242k of cumulative rental profit. At 47%: $114k in tax never paid.

Year 29. Reserve depletes.

Yes, you read that correct. You receive 12 years of TAX FREE rental income.

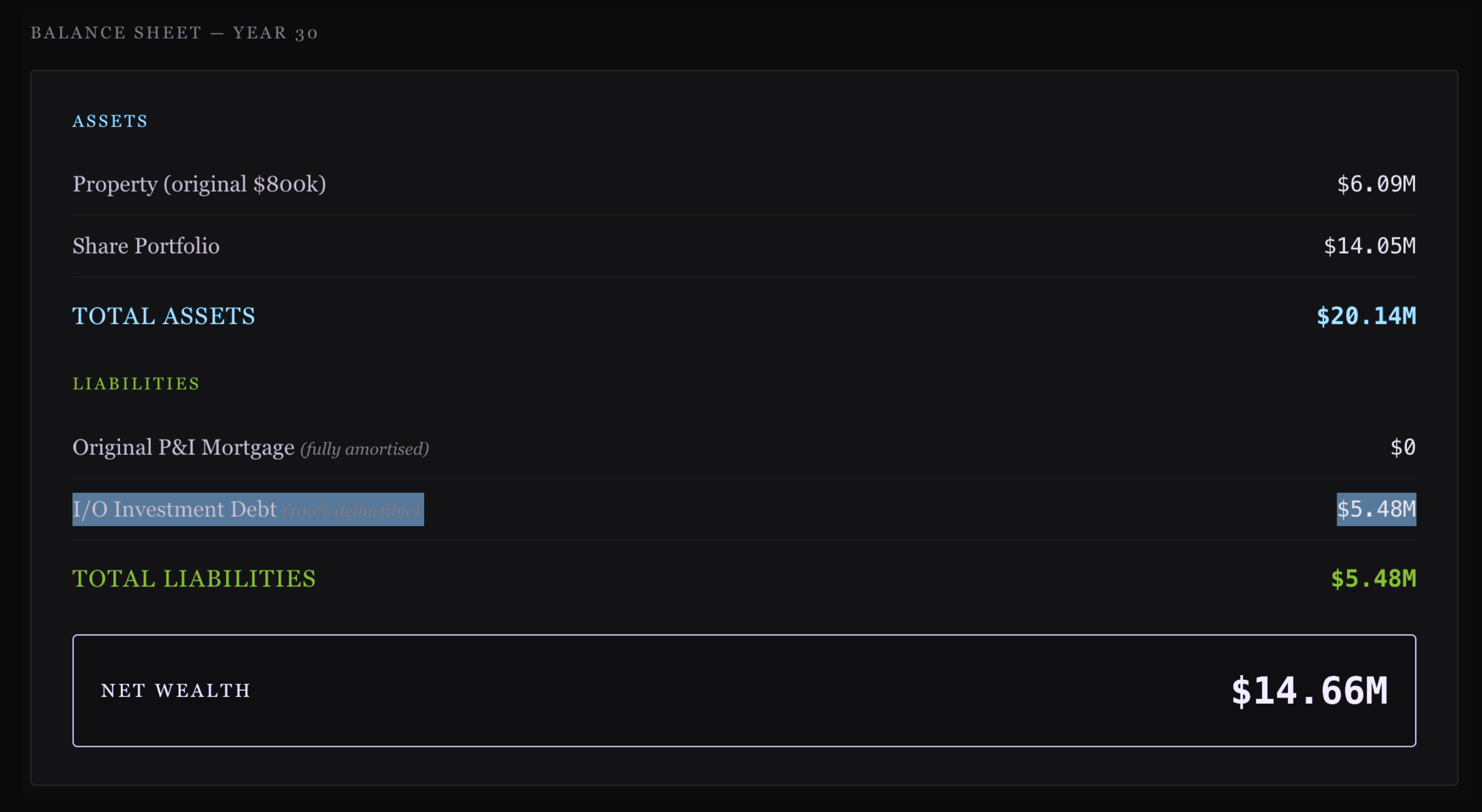

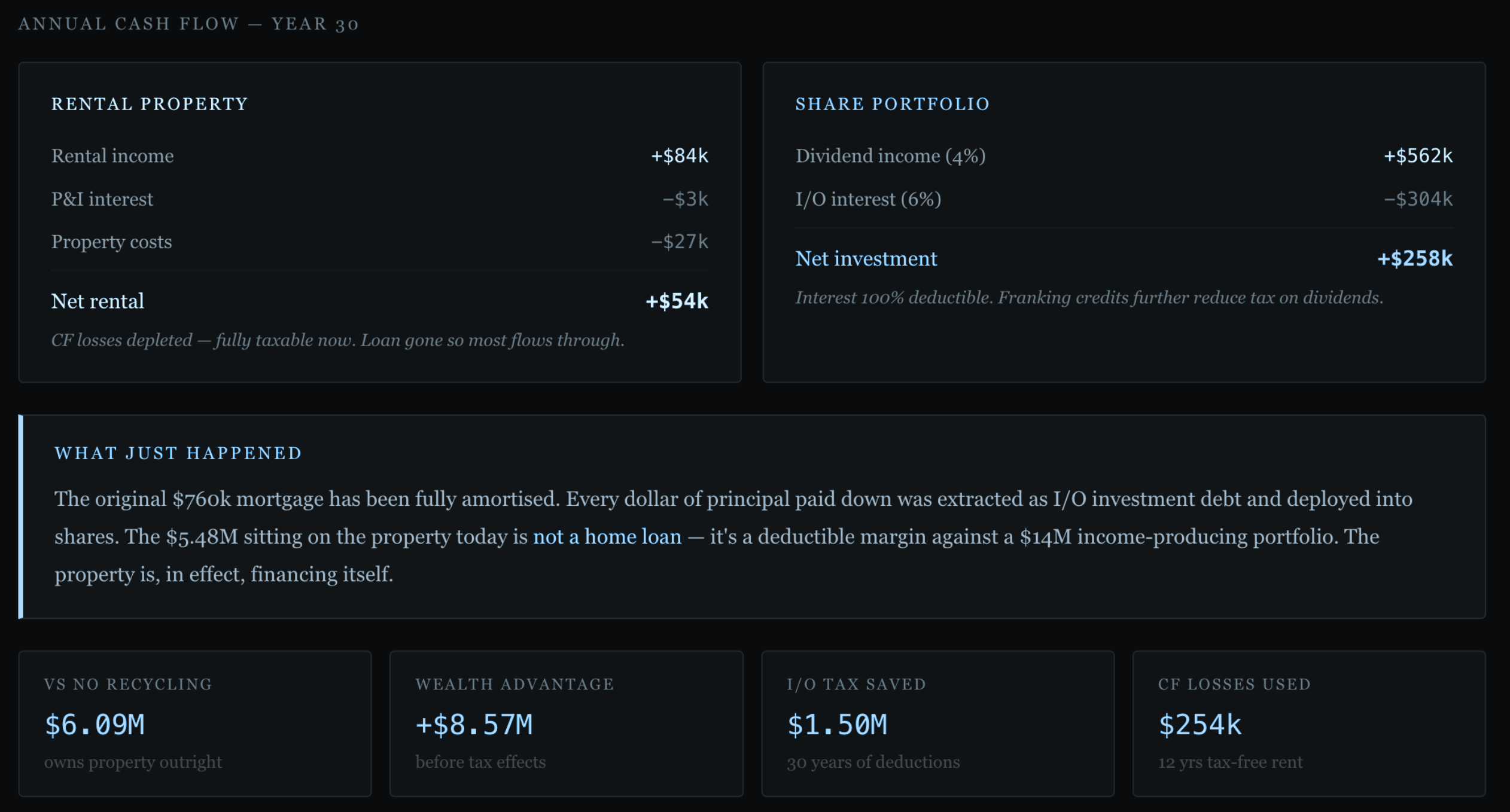

Year 30. P&I loan fully paid off.

The original mortgage being gone isn’t exciting

The $5.48M Debt now sitting on the property is.

Fully tax deductible.

Against a $14.05M share portfolio.

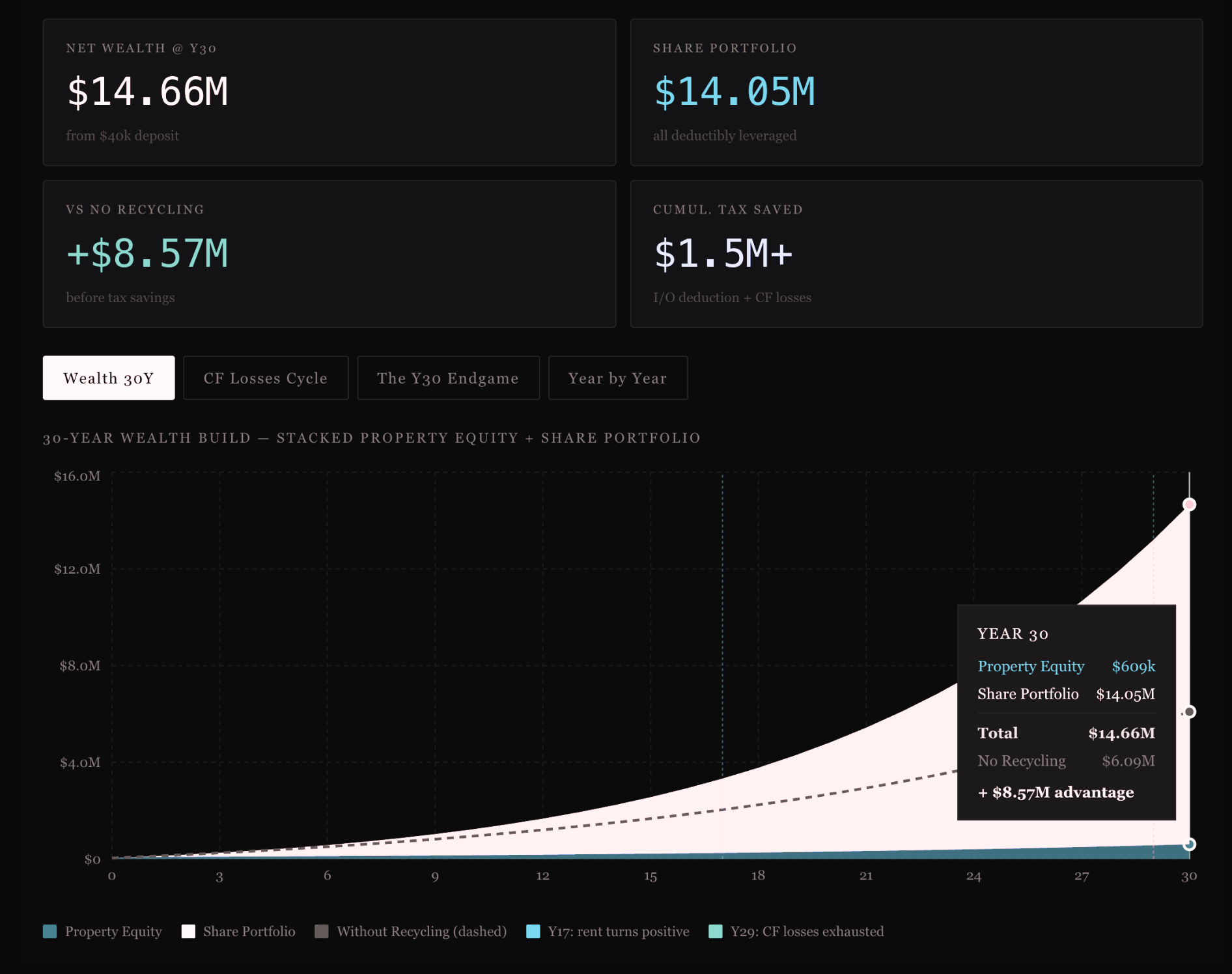

The Year 30 Balance Sheet

Net Wealth: $14.66M

From a $40k deposit.

The same person who buys the same property and pays it off the conventional way ends Year 30 with $6.09M net wealth.

The recycling strategy adds $8.57M, and roughly $1.5M in cumulative tax savings.

A $10M advantage.

What if they want to buy more than one property?

Each additional property accelerates the leverage and debt recycling engine.

More principal being paid down. More equity being extracted.

More investment debt. More deductions. More shares compounding.

The Real Opportunity

Clients getting proper advice will buy the right asset, with the right structure, with the right loan splits, with the right timing.

This strategy is simple.

Buy with the 5% Deposit Scheme. Live in it. Pay it down. Rentvest.

Extract above 90% LVR (LMI eligble professional. If not eligble it’s 80%. )

Recycle into shares. Bank the losses.

Wait for the property to flip positive.

Watch the losses absorb the rental income tax-free.

Pay off the original mortgage.

End up with an investment-grade balance sheet, not a paid-off house.

That is the opportunity.

Not for everyone. Not for every property. Not without risk.

Not for the unadvised.

While past results do not guarantee future outcomes, our 5% Deposit first home buyer acquisitions for over 5 years have shown us how powerful the right asset selection and structure can be when executed properly.

While everyone else argues about the budget, my job is to figure out:

How do you build wealth when the old shortcuts stop working?

We are already reviewing this with our clients.

We have two other strategies that could be even more transformational if these policies go through.

The people who get advice early will not just react to the rules.

They will restructure around them.

Want a tailored strategy as a first time buyer or existing investor?

Option 1 - Book a call for a tailored strategy built around your numbers.

Option 2 - Reply to this email to secure a ticket to our post budget strategy event on the 27th of May @ 6PM AEST.

Who is advising you?

ASSUMPTIONS COMPOUND OVER 30 YEARS:

$800k purchase, 5% deposit, $760k P&I @ 6% over 30yr. LMI waiver refinance at 10% to exit scheme, 7% p.a. property growth, 8% p.a. share return, 3.5% initial yield growing 4% p.a., $12k holding costs growing 3% p.a., 47% marginal tax rate, full extraction of equity above 90% LVR each year deployed as I/O debt into shares. Past performance does not guarantee future results. Assumes consistent legislation, market conditions, employment, lending criteria, and discipline of execution. All assumptions drift in real markets. Errors in modelling can occur and averages are not a reflection of how life works. Rates go up, rates go down. As does everything in life.

For illustrative purposes only. Not financial advice.

Consult me as a licensed adviser, our lending specialist and an accountant/ or your own team before acting.